What should a federal employee do with their Thrift Savings Plan when the market is going down like it has been? Is it a good time to cut losses and move it all to the G fund? This was a major question in 2008 and 2009 and has once again made a comeback.

Before clicking that button to move everything to the G fund, I believe there are a couple of questions that you need to answer first.

- Why am I moving my money to the G fund?

- When will I move money back into the stock funds?

The most common answers I get from those questions are:

- I’m scared and I don’t want to lose anymore.

- I don’t know, but I want to wait for things to calm down.

Why am I moving my money to the G fund?

Let’s start with ‘I don’t want to lose anymore.’ This isn’t a strategy but more of an emotional reaction, and emotional reactions have no place in an investment plan. Before anyone invests in stocks, they need to understand that there is volatility involved. It’s par for the course. Stocks (or mutual funds made up of stocks) don’t go up in a straight line unless there is a guy named Bernie behind them!

In reality, your account value will fluctuate over time. Most long-term investors will experience at least a handful of down markets over the course of their lifetime. If you are working with an advisor, they should be able to show you what this looks like. If you are doing it on your own, I encourage you to do some research on market drawdowns and take note of the dollar impact that this will have on your investments.

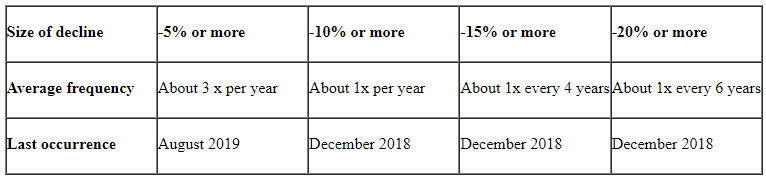

If you can’t handle seeing your account fluctuate, then you probably shouldn’t be invested in stocks at all. Here is some information that I saw recently about market downturns and their frequency.

Sources: Capital Group, Standard and Poor’s

You can see from the chart above that most decades will have at least one stock decline of 20% or more. Our most recent drawdown is already over 20%.

If moving your money in and out of the G fund is part of your strategy, then you should have a good answer to the question below.

When do you get back in?

Getting back into market is the toughest part of getting out. Once you get out, you really need to know where the bottom is going to be in order to get back in. If you think the market is going down 20% and it only goes down 15% and goes back up from there, you have just missed out and negated the move out of the market.

To help prove my point I’d like to share a story of a famous investor and my own experience.

The Buffet Bet

Many of you may recall that Warren Buffet made a million-dollar bet in 2007 with a hedge fund manager. The bet was that the S&P 500 would outperform a basket of at least five hedge funds over the next decade. The decade started in 2008 and ended in 2017.

Hedge funds typically try to make money in any kind of market environment, or at the very least they attempt to protect money when the market is going down and make money while it’s going up. Knowing that, you would think the time frame would be perfect for a hedge fund to beat an index. Also, note that most hedge fund managers are very bright individuals, many of whom have earned a PhD., have advanced mathematics degrees, etc.

Despite having a drawdown of over 50%, the S&P 500 made over 85% in the decade while the average hedge fund that was picked made just 22%. The best of the five hedge funds gained 62.8%.

Keep in mind that we are comparing investing, and staying invested in a stock index to some of the more sophisticated investments that you can find, being managed by some of the brightest minds in the investment world, and the boring index won by a ton! Not even the best of the five beat the index.

My experience during 2008 drawdown

From 2008 to 20012, I probably did around 80 seminars for federal employees throughout the Midwest. The question I was asked everywhere I went was, “what do I do with my TSP?” And the most common thing I was told in 2008 and yes, 2009 was, “I couldn’t handle it anymore, I moved everything to the G fund.” I don’t recall one person telling me that they were moving all of their money to the stock funds in that time period.

Fast forward to 2011 and 2012 and it was still common for someone to approach me and say that they moved everything to the G fund in 2009 and have been sitting on the sidelines waiting for the right time to get back in.

After reading my experience above and Buffet’s Bet, my questions are:

- Are you smarter than hedge fund managers?

- How did you react to the drawdown in 2008 through the beginning of 2009?

The first question isn’t meant to be funny, but a serious question. If hedge fund managers with advanced degrees on the subject can’t beat a simple index, then why would the average federal employee expect to?

Your reaction to the last market downturn will tell you a lot about risk tolerance; however, people’s risk tolerance can change as they get older and experience different life events.

What should you do?

If you work with an advisor, this is the time where they prove their worth. Call and talk about your concerns and get some feedback. Sometimes people enter a different stage of life or have had lifestyle changes that warrant an allocation change. The time for this change may not be after a 25% market drop, though. Maybe you should rebalance and buy some stocks and sell bonds? If you are still saving, maybe you want to invest some cash now.

There are a number of actions you could take right now, but the most prudent action may be to do nothing. Stay put.

Market drawdowns can be very nerve wracking, but they don’t have to be. Make sure you understand your long-term goals and invest accordingly. If you find times like these especially rough, it may be time to seek the help of a qualified advisor. If you would like to have a conversation and see if we are a good fit, schedule an introductory call. I’d be happy to talk with you and discuss your options.