Life insurance tends to be a touchy subject. Some people don’t want to discuss death and others just “don’t believe in insurance.”

Most federal employees I talk to will carry life insurance in their younger days, but don’t plan on having any in retirement. But are those intentions well thought out?

Full disclosure – I am a FEE-ONLY financial advisor. This means that I DO NOT sell any life insurance or earn any commission for doing so. In other words, I have no dog in this fight other than to inform feds who are headed into retirement what financial options are in their best interest.

As far as the “I don’t believe in life insurance” argument goes, there isn’t much time to be wasted here. Believe in? When I hear “believe in” I think of my faith and maybe a few people, but “believing in” a product? Owning life insurance has nothing to do with believing in a product. It has to do with loving someone. If you love someone enough, then you may consider carrying life insurance to financially protect them in your absence.

Why would I need life insurance in retirement?

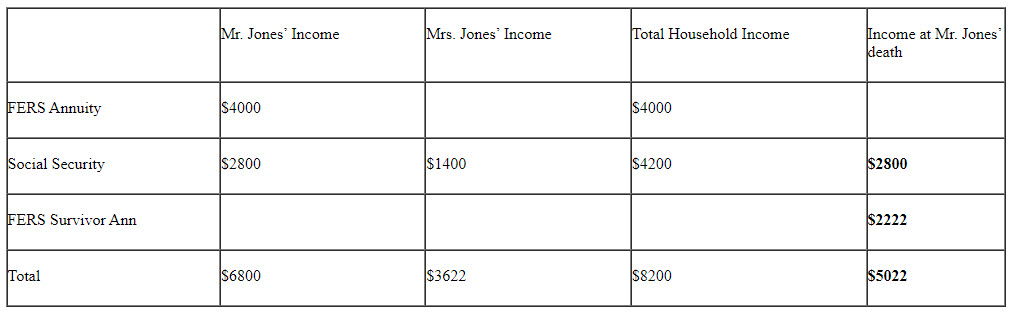

Why to carry life insurance in retirement is pretty simple. In the event one spouse dies, the surviving spouse could be left with significantly less income.

The Jones family’s current monthly income is $8,200. If Mr. Jones passes tomorrow, then Mrs. Jones is left with a monthly income of $5,022 (FERS survivor annuity of $2,222 plus $2800 Social Security). This comes out to a 39% reduction in income for Mrs. Jones. While expenses may drop a little at the passing of one spouse, the same 39% reduction in expenses isn’t likely. An income change of 39% would require some significant life changes for the grieving Mrs. Jones.

How does TSP affect this scenario?

Notice that I didn’t include income from TSP in either scenario. The main concern is the guaranteed income being reduced. Investment income isn’t going to be any different if it’s for one person or two.

But, retirees that enter into retirement without enough life insurance may need to be more conservative with their TSP withdrawals. What do I mean by conservative? If a couple enters retirement with plans to travel, spoil grand kids, and other scenarios that take money to do, they may not be able to do those things if the surviving spouse would have less income as a result.

Looking at the example above, the Jones’s may need to delay TSP withdrawals in order to give the TSP more time to grow. This way, Mrs. Jones can receive a higher income in the absence of life insurance benefits.

For example, if the Joneses retire with a TSP balance of 700k, they would receive an income of $28,000 a year using the 4% rule. If they delay distributions for 10 years and the TSP averages 7% growth per year, their TSP could grow to 1.4 million.

This strategy could potentially double Mrs. Jones income from TSP if Mr. Jones passes first. But again, this would require 10 years of taking no income and making a 7% return per year.

What if they had life insurance?

If the Joneses had a life insurance policy for 500k (an example) on Mr. Jones, then they could spend more freely. Having the life insurance policy gives them the security of knowing that Mrs. Jones will not take a reduction of 39% in income should Mr. Jones pass. Now they can spend more freely while they are both alive.

Do you need life insurance in retirement?

Don’t rule it out. Everyone is different so it’s going to depend on your financial situation as well as your own wants and needs. Life insurance is a bigger need for couples with large disparities in guaranteed income. A perfect example is the high earning federal employee whose spouse stayed home most of their life to raise kids.

Despite what some life insurance salesman may claim, insurance isn’t the answer to everything, but it does fit a need. Evaluating life insurance needs is another part of the financial planning process. If you are nearing retirement and want help trying to figure things out, schedule a call and see if we can help.

Brad Bobb, CFP® is the owner of Bobb Financial Inc, and an expert in retirement planning for federal employees.